HSBC Revolution Credit Card: Great for Online and Social Spend

HSBC Revolution Credit Card: Great for Online and Social Spend

ValueChampion Rating ![]()

Pros

- Great rewards on local dining and entertainment

- Online shopping perks

- No-fee card

Cons

- Lacks rewards for frequent travellers who spend large amounts overseas

- Not suitable for low budgets

HSBC Revolution Credit Card is great for social spenders who shop online and prefer to avoid annual fees. On top of zero annual fee, you can also earn up to 4 miles, equivalent to up to 10X reward points or up to 2.5% cashback, for every S$1 spent on all online and contactless payments. Everything else including overseas spend earns you 0.4 miles, so HSBC Revolution Card is best for social and online spenders with budgets of S$1,000+ per month.

HSBC Revolution Card Features and Benefits

|

|---|

Key Features:

|

Our Evaluation: Flexible Rewards on Online and Contactless Purchases

HSBC Revolution Credit Card could be one of the best credit cards in Singapore for contactless payment and online purchases. Here's why.

HSBC Revolution Credit Card offers consumers an easy way to maximise rewards for contactless spend and online shopping without paying a high annual fee. Cardholders earn an unlimited 4 miles per S$1 spend on online and contactless payments (Visa payWave, Apple Pay and Google Pay), equivalent to 10X Rewards points or 2.5% cashback.

While consumers can quickly earn miles from HSBC Revolution Credit Card's online and contactless rewards rates, all other categories–including overseas–receive just 0.4 miles per S$1 spend. Despite offering access to lifestyle and travel discounts, HSBC Revolution Card is not the best fit for diversified spenders or frequent travellers.

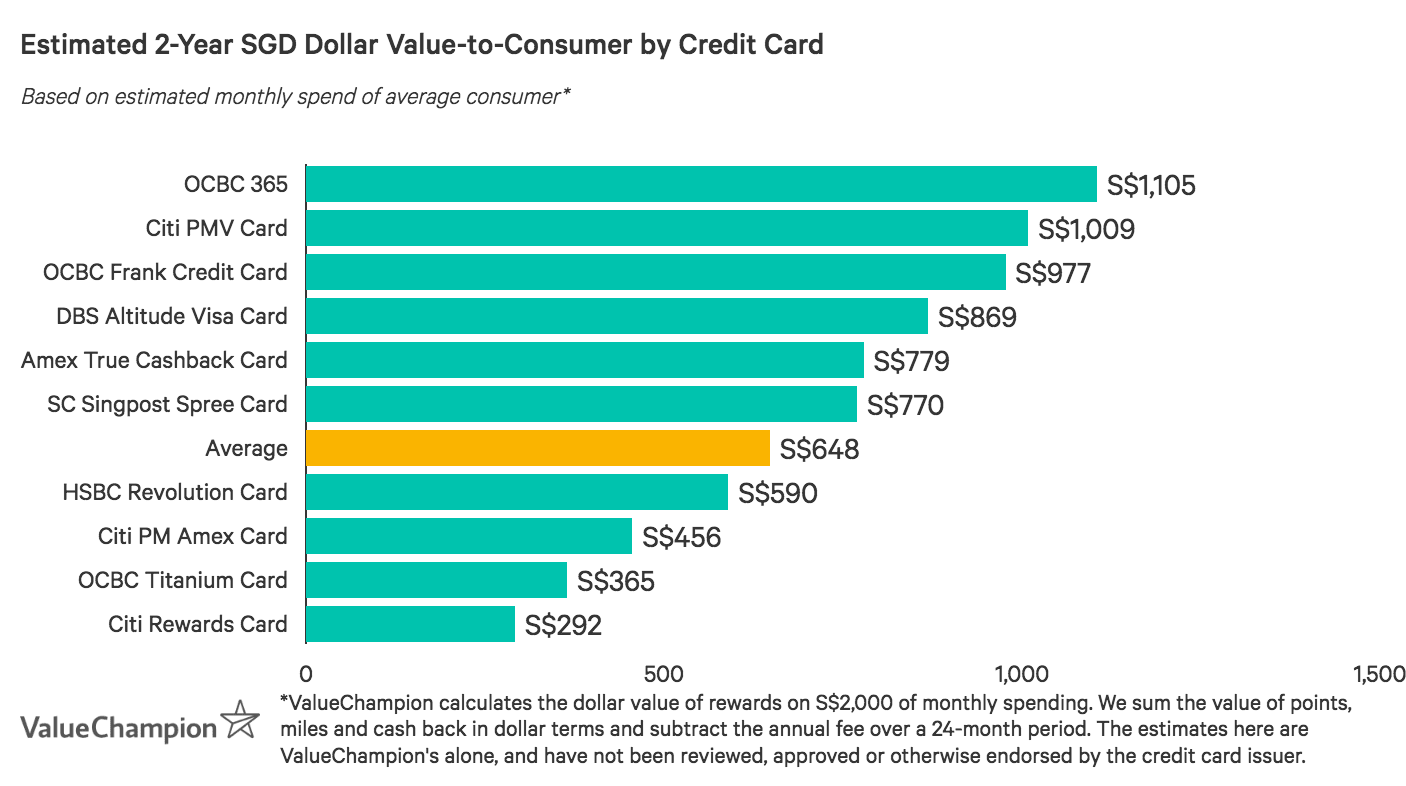

Individuals who shop online and and pay via mobile apps are most likely to benefit from HSBC Revolution Credit Card. Since the rewards points are capped at 9,000 rewards points on eligible transactions, customers who spend at least S$900 online and on contactless payments will find this card most beneficial.

How HSBC Revolution Credit Card's Rewards Program Works

HSBC Revolution Credit Card offers 10X rewards points on eligible transactions, which include mobile and contactless spend. This can be broken down to 9X bonus points and 1 base point per S$1 spend. All other transactions earn 1X reward point per S$1 spend. While the base points are not subject to a monthly cap, bonus points are capped at 9,000 points per calendar month. This translates to 3,600 miles per month on eligible transactions, which require at least S$900 monthly spend on online and contactless purchases.

Use our quick guide below to learn how you can redeem HSBC Revolution Credit Card rewards.

- Spend earns Rewards Points (redeemable as vouchers, miles or cash credit)

- Cash credits can be redeemed in blocks of S$50 and S$100

- Cardholders must pay an annual fee of S$40 to partake in Mileage Programme (Asia Miles & KF)

- Points can be redeemed for miles through Mileage Programme in blocks of 10,000 Points for 4,000 miles

- Points expire 3 years after they are earned

Before You Apply: Fees, Limits, and Exclusions

The following credit card expenditures are ineligible for cash back or rebate.

Examples of excluded transaction include:

- Foreign exchange transactions (including but not limited to Forex.com);

- Donations and payments to charitable, social organisations and religious organisations;

- Payments on money payments/transfers (including but not limited to Paypal, SKR skrill.com, CardUp, SmoovPay, iPayMy);

- Payments to any professional services provider (including but not limited to GOOGLE Ads, Facebook Ads, Amazon Web Services, MEDIA TRAFFIC AGENCY INC);

- Top-ups, money transfers or purchase of credits of prepaid cards, stored-value cards or e-wallets (including but not limited to EZ-Link, Transitlink, NETS Flashpay and Youtrip);

- Payments in connection with any government institutions and/or services (including but not limited to court costs, fines, bail and bond payment);

- Any AXS and ATM transactions;

- Tax payments (except HSBC Tax Payment Facility);

- Payments for cleaning, maintenance and janitorial services (including property management fees);

- Payments to educational institutions;

- Payments on utilities;

- The monthly instalment amounts under the HSBC Spend Instalment;

- Balance transfers, fund transfers, cash advances, finance charges, late charges, HSBC’s Cash Instalment Plan, any fees charged by HSBC;

- Any unposted, cancelled, disputed and refunded transactions

How does HSBC Revolution Credit Card Compare Against Other Cards?

Read our comparisons of HSBC Revolution Credit Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need.

HSBC Revolution Credit Card v. Citi PremierMiles Visa Credit Card

- Pros

- Frequent traveler perks

- Low fees

- Flexible miles redemption

- Cons

- Lacks luxury perks

- Not suitable for occasional travel

Casual travellers with diversified spend can benefit from Citi PremierMiles Visa Credit Card. Citi PMV Credit Card incentivizes overseas spend with 2 miles per S$1 (compared to 0.4 miles with HSBC Revolution Credit Card) and offers travel perks like free travel insurance and airport lounge access. Its 1.2 miles per S$1 local spend rate is also higher than HSBC Revolution Credit Card's. However, the credit card's S$192.6 fee is waived 1-year only, and local spenders with social spend behaviors could potentially earn more with HSBC Revolution Credit Card.

HSBC Revolution Credit Card v. OCBC Titanium Rewards Credit Card

- Pros

- 10 pts (4 miles) per S$1 on fashion & select retail (Qoo10, Amazon, & more)

- Fee waiver with S$10,000 annual spend

- Cons

- 1 pt (0.4 miles) per S$1 other spend

- Earnings capped at 48,000 miles per year (worth S$480)

Fashion retail shoppers can avoid annual fees with OCBC Titanium Rewards Credit Card, which rewards 4 miles per S$1 shopping spend on clothes, shoes, bags, and more online and offline, locally and overseas. While HSBC Revolution Credit Card offers less for offline shopping spend, it rewards a wider variety of online spend, from travel bookings to EZ-Link top-ups (though at 2 miles per S$1 spend). Like HSBC Revolution Credit Card, OCBC Titanium Rewards has a waivable fee, but with a lower required annual spend (S$10,000). For fashionistas, OCBC Titanium Rewards Credit Card may be the better option.

HSBC Revolution Credit Card v. Maybank Horizon Visa Signature Credit Card

- Pros

- High spend on local dining & transport

- Great for local spend and miles rewards on travel

- 3 years fee waiver

- Cons

- Doesn't reward overseas spend

- Few travel perks & privileges

- Lacks in rewards for essentials (ie groceries)

Maybank Horizon Visa Signature Card is a great fit for local diners and frequent travellers, offering up to 3.2 miles per S$1 spend on local dining, petrol and taxi fares and 2 miles for air tickets, travel packages and overseas spend. These rates are higher than HSBC Revolution Credit Card's, but require a S$300 minimum monthly spend. In addition, earnings are capped at 12,000 miles/month, but this is fairly high. Both credit cards have waivable fees but Maybank Horizon Visa Signature Credit Card requires a higher annual spend (S$18,000). Ultimately, this card benefits travellers while HSBC Revolution Credit Card prioritises local spending.

HSBC Revolution Credit Card v. DBS Altitude Visa Credit Card

- Pros

- Great for online travel bookings

- Cons

- Those willing to pay an annual fee for more bonus miles

- Affluent travellers who are willing to pay a high fee for luxury travel perks

Consumers spending closer to S$2,100 per month can earn more for diversified spend with DBS Altitude Visa Credit Card. While the annual spend requirement for a fee waiver is high at S$25,000, consumers earn 1.2 miles per S$1 local spend, 2 miles overseas, and 3 miles for online travel bookings. Cardholders also receive free travel insurance, airport lounge visits, golfing discounts and more. HSBC Revolution Credit Card is by comparison a bit limited and offers less to travellers. However, its annual fee is waived with just S$12,500 in annual spend, making it more accessible to some consumers.

Methodology: How We Evaluate Credit Cards

Our analysis of consumer credit cards involves calculating the total value of a card's rewards rates, bonuses, and discounts minus the cost of its annual fee, rewards caps, and required spend. Temporary promotions and intangible perks are considered, but do not necessarily enter the equation when we calculate final value.

ValueChampion makes certain assumptions when estimating the rewards value of credit cards. These matter because most cards offer different cashback or miles rates based on the type of spend involved. Our profiles reflect a best guess at the spend decisions of a typical consumer on an average budget.

If you would like to see how our calculations work on your own budget, head over to our RealValue Rewards Calculator and type in how much you spend in various categories to see an instant comparison of the predicted rewards value of dozens of cards.

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.