Average Cost of Home Loans 2024

With the hike in interest rates for property loans in Singapore, some homeowners might want to consider refinancing their mortgage loans to fight against the increase. You can check out PropertyGuru's SmartRefi tool today to find out how much you can save from refinancing your mortgage loan:

Taking out a home loan is one of the biggest financial decisions individuals make in their lives. Given that homes in Singapore are some of the most expensive in the world, the loans that finance them can have a huge impact on the consumer's wallet. Here, we discuss the average cost of home loans in Singapore, and break it down to different components like interest rates and refinancing fees. When shopping for a home loan, you can reference these to assess the offers you receive from your banks.

- Average Interest Rates of Home Loans

- Factors That Influence Cost of Home Loans

- Average Cost of Refinancing

Average Interest Rate of Home Loans in Singapore

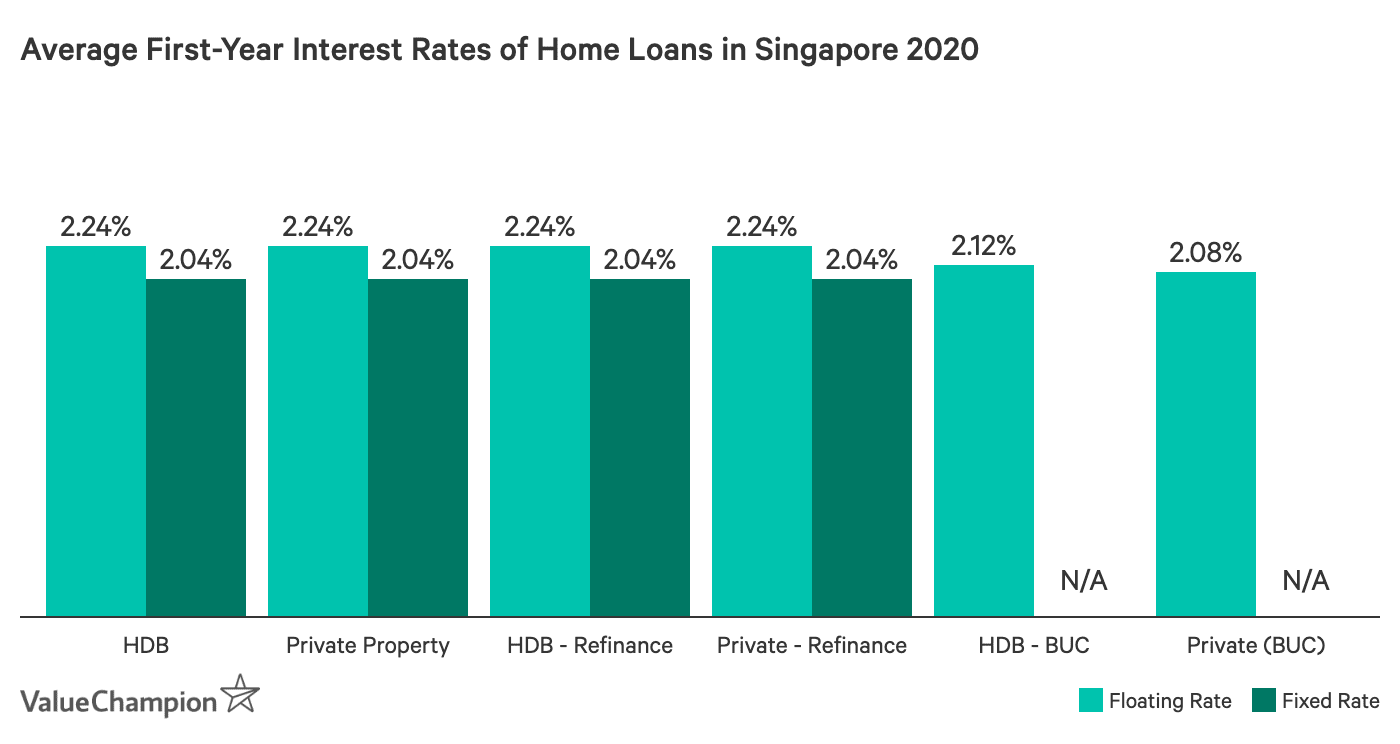

As of March 2022, we found that the average interest rates of home loans in Singapore ranged between 0.80% to 2.50%, with most bank charging below 2%. This rate can vary depending on whether your property is a HDB flat, a private residence, or a building under construction. Not only that, rates can be different for home loans that are used to refinance an existing home loan. Below, we demonstrate average interest rates of home loans by category. Compared to these average rates, the best home loans in Singapore can help you save a significant amount in interest payments.

Rest Rate vs Flat Rate

It’s important to understand that home loans in Singapore are priced with “rest” interest rates, as opposed to “flat” interest rates. In contrast, car loans tend to be priced with flat rates. The difference between the two rates is that flat rates tend to be more expensive than rest rates because of the way they are calculated. Let’s examine this difference in detail.

Let’s consider a home loan of S$500,000 over 30 years with a rest interest rate of 1.5%. Because a home loan in Singapore is priced with a “rest” interest rate, your interest expenditure is calculated based on the remaining balance of your loan after each month. This means that your monthly payment will be about S$1,726, which consists of an increasing amount of principal and decreasing amount of interest payment over time. Because the interest rate is applied only to the remaining balance (as opposed to the beginning balance for flat rates), you end up paying only S$121,216 in interest over 30 years.

| Rest Rate | |

|---|---|

| Principal | S$500,000 |

| Interest Rate | 1.5% |

| Tenure | 30 Years |

| Monthly Installments | S$1,726 |

| Total Interest Payment | S$121,216 |

Now, consider a car loan of S$500,000 over 30 years with a flat interest rate of 1.5%. Because this car loan comes with a “flat rate,” your interest is a “flat,” constant payment of S$500,000 x 1.5%, which translates to S$7,500 of interest expense each year. Your monthly instalment will be a constant amount consisting of S$625 (S$7,500 divided by 12 months) plus a principal payment of S$1,389 (S$500,000 divided by 360 months). After 30 years, you will have repaid your debt in full after having paid S$225,000 in interest, about double what you would have paid for a rest rate loan. The key principle to understand here is that interest payment is kept “flat” no matter how much money you repay.

| Flat Rate | |

|---|---|

| Principal | S$500,000 |

| Interest Rate | 1.5% |

| Tenure | 30 Years |

| Monthly Installments | S$2,014 |

| Total Interest Payment | S$225,000 |

How Fixed Rates & Floating Rates Work

Home loans are largely priced at fixed interest rates or floating interest rates. Fixed rate mortgage loans charge you a fixed interest rate for up to 3 years, though a small number of home loans only do this for 1-2 years. After the 3rd year, banks start charging you a floating rate. Floating interest rates fluctuate regularly because they are pegged to a pre-designated reference rates like Singapore Overnight Rate Average (SORA) and fixed deposit rates. Therefore, if the market interest rate continues to rise when you have to pay a floating rate, your monthly instalment will also increase. In Singapore, majority of the banks use SORA as their reference rate.

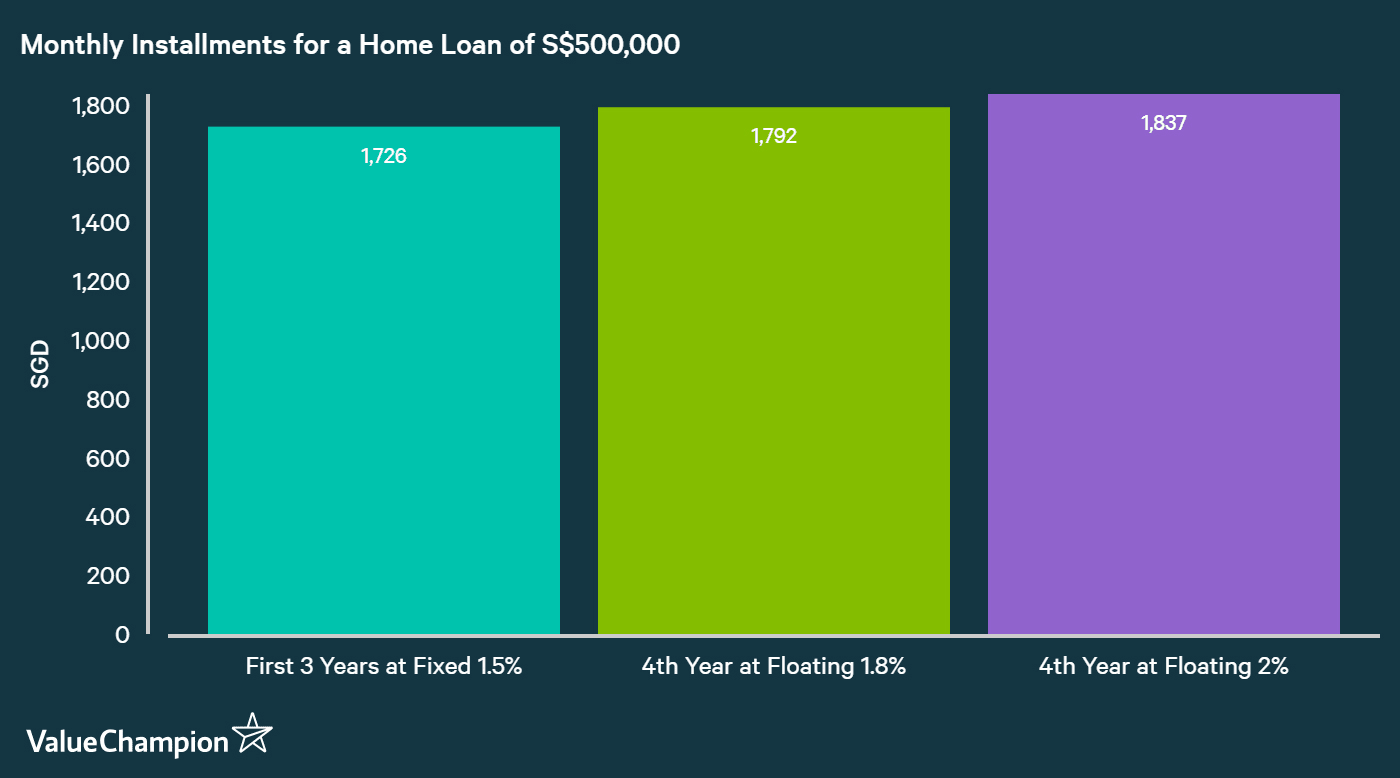

For example, let's assume you take out a fixed rate home loan of S$500,000 with a tenure of 30 years. In order to get this loan, you agree to pay a fixed annual interest rate of 1% to the bank. By the end of the 3rd year, you will have paid total of S$14,368 in interest and S$43,527 in principal.

Then, you choose to refinance the remainder your loan (S$500,000 - S$43,527 = S$456,473) at a rate that's pegged to the SORA rate at the time, which we assume for now to be around 0.3% since rates are set to rise. Then, for the duration of the loan, you will be paying a total interest of 0.3% (SORA) plus an additional interest rate indicated separately by each bank. These range currently around 0.8% to 1.5%. Assuming that the bank additional interest rate is 1.5%, the total will be 1.8% which roughly translates to S$1,780 of monthly installments.

One notable characteristic of floating rates is that it can change constantly as the reference rates fluctuate. Because most floating rates are pegged to SORA, thus if SORA in our example increases during the 12-month period, then so will your interest rate on your loan. Therefore, if SORA increases by 0.2% during your 12-month period, then your monthly installment can increase to S$1,837.

Fixed Rate vs Floating Rates: Which Is Better?

When choosing between a fixed rate home loan and a floating rate home loan, you should really focus on getting a good grasp on how rates will behave in the next 2 to 4 years while your loan is locked up. Because you can refinance your loan quite easily after 3 years, a longer time horizon is less relevant (and impossible to predict in the first place). Below, we discuss a few possible scenarios that you must consider, and whether fixed or floating rate is more preferable in each of the situations.

Flat to Declining Interest Rates

When market interest rates are stable or declining, it tends to be more beneficial to choose a floating rate home loan. In a stable rate environment, floating interest rates tend to be lower than fixed rates because banks are willing to take a lower rate for the opportunity to earn more money as soon as rates begin to move upwards. A fixed rate, on the other hand, will guarantee a certain rate for the borrower for a long time, so banks charge a premium for these in low-rate environments. Therefore, getting a floating rate can help you pay less in interest and potentially even benefit when rates decline. In the table below, we show the approximate difference in average floating rates and fixed rates for new home loans as of March 2022.

| Property Type | Average Fixed Rate | Average Floating Rate |

|---|---|---|

| HDB | Approximately 1.38% | Approximately 1.13% (Inclusive of March 2022 SORA) |

| Private | Approximately 1.38% | Approximately 1.13% |

| HDB Concessionary Interest Rate | 2.60% | |

Rising Interest Rate

When overall interest rates are rising, it's generally more advisable to take out a fixed rate home loan than a floating rate loan. Although fixed rates tend to be a bit higher than floating rates, they can help save money when market rates rise in a meaningful way. For instance, consider a hypothetical scenario where you have the option of paying 1.5% in fixed rate for the next 3 years and another option of paying a floating rate of 1% for now. Soon after you take out the loan, central banks all over the world decide to begin raising their interest rates. This means that, by the second year, you might end up paying 2% to 2.5% in floating rates while your fixed rate is still only 1.5%. A difference of 1% for a loan of S$500,000 translates to difference of S$5,000 in annual interest you are paying to the bank.

Factors That Influence Cost of Home Loans

The total cost of a home loan can be influenced by multiple factors. The core principle here to understand is that banks, as any business, wants to maximise profit while minimising losses. Therefore, they tend to offer lower costs for big, profitable deals. The flip side is that they charge higher rates for deals that have greater probability of loss than average in order to compensate for the risk. Below, we discuss each of the major factors so you have a better understanding of how it works.

Find the Cheapest Home Loans in Singapore

Market Rate

As we discussed above, all home loans in Singapore behave like a floating rate at some point in their tenure. Therefore, it's generally a good practice to keep an eye out for how market rates are behaving. Generally, the most important rate to monitor is SORA. Most bank loans are pegged to SORA, so if this rate goes up, the cost of your home loan will increase as well. Therefore, it's generally a good practice to lock-in a low interest rate when SORA is near historical low.

Market Value, Leverage

How much you borrow to buy your home will also affect the cost of your home loan. This works through a multiple mechanism. First, more expensive homes tend to have lower interest rates. Think of it as a wholesale practice where banks give you a preferential rate to win a big business. For some home loans of more than S$1.5mn, banks will even be willing to negotiate their rates further down.

Another mechanism that is worth discussing is leverage. Leverage essentially refers to how much someone has borrowed relative to his income and net worth. In terms of home loans, we measure leverage in two ways: Loan-to-Value ratio (LTV) and Total Debt Servicing Ratio (TDSR).

LTV ratio is the ratio of amount of home loan taken relative to the value of the home. For example, if you borrow S$500,000 to buy a S$1,000,000 HDB flat, your LTV is 50%. The higher the ratio, the more leverage you have. Banks generally prefer lower LTV ratios because it means less risk for the bank to lose money. In our example, if you default on your loan, the bank can simply sell your home at a 50% discount to recover their money. However, if your LTV ratio is 80%, it's more difficult for the bank to recover their money as they have to try and sell your home at a 20% discount. Generally, banks will tolerate LTV ratios of up to 80% at max. Below is a summary table of various LTV requirements.

| Maximum LTV Ratio | Conditions | |

|---|---|---|

| 75% | Purchasing a HDB flat, no outstanding housing loan: | • the tenure does not exceed 25 years; and |

| • the sum of the loan tenure and the age of the borrower at the time of applying for the loan does not extend beyond retirement age of 65 years. | ||

| Purchasing a private property, no outstanding housing loan | • the tenure does not exceed 30 years; and | |

| • the sum of the loan tenure and the age of the borrower at the time of applying for the loan does not extend beyond retirement age of 65 years. | ||

| 55% | Purchasing a HDB flat, no outstanding housing loan: | • the tenure exceeds 25 years (up to a maximum of 30 years); or |

| • the sum of the loan tenure and the age of the borrower at the time of applying for the loan extends beyond retirement age of 65 years. | ||

| Purchasing a private property, no outstanding housing loan: | • the tenure exceeds 30 years (up to a maximum of 35 years); or | |

| the sum of the loan tenure and the age of the borrower at the time of applying for the loan extends beyond retirement age of 65 years. | ||

| 45% | Purchasing a HDB flat, 1 existing outstanding housing loan: | the tenure does not exceed 25 years; and |

| the sum of the loan tenure and the age of the borrower at the time of applying for the loan does not extend beyond retirement age of 65 years. | ||

| Purchasing a private property, 1 existing outstanding housing loan: | • the tenure does not exceed 30 years; and | |

| • the sum of the loan tenure and the age of the borrower at the time of applying for the loan does not extend beyond retirement age of 65 years. | ||

| 35% | Purchasing a HDB flat, 1 existing outstanding housing loan: | • the tenure exceeds 25 years (up to a maximum of 30 years); or |

| • the sum of the loan tenure and the age of the borrower at the time of applying for the loan extends beyond retirement age of 65 years. | ||

| Purchasing a private property, 1 existing outstanding housing loan: | • the tenure exceeds 30 years (up to a maximum of 35 years); or | |

| • the sum of the loan tenure and the age of the borrower at the time of applying for the loan extends beyond retirement age of 65 years. | ||

| 25% | Purchasing a HDB flat, 2 or more existing outstanding housing loans: | • the tenure does not exceed 25 years; and |

| • the sum of the loan tenure and the age of the borrower at the time of applying for the loan does not extend beyond retirement age of 65 years. | ||

| Purchasing a private property, 2 or more existing outstanding housing loans: | • the tenure does not exceed 30 years; and | |

| • the sum of the loan tenure and the age of the borrower at the time of applying for the loan does not extend beyond retirement age of 65 years. | ||

| 15% | Purchasing a HDB flat, 2 or more existing outstanding housing loans: | • the tenure exceeds 25 years (up to a maximum of 30 years); or |

| • the sum of the loan tenure and the age of the borrower at the time of applying for the loan extends beyond retirement age of 65 years. | ||

| Purchasing a private property, 2 or more existing outstanding housing loans: | • the tenure exceeds 30 years (up to a maximum of 35 years); or | |

| • the sum of the loan tenure and the age of the borrower at the time of applying for the loan extends beyond retirement age of 65 years. |

TDSR is total monthly debt obligations (i.e. combined interest and principal repayment on your home loan, car loans, personal loans, credit card debt, etc.) divided by your monthly income. This is meant to measure one's ability to repay his debt obligations every month. Generally, TDSR cannot exceed 60% and banks will not lend HDB home loans to people who have TDSR of greater than 30%. Higher TDSR means higher risk for the bank, so generally will translate to higher interest rate for the borrower.

Credit Score

Your credit score will have an impact on banks' willingness to lend to you, and hence the interest rate that that they are willing to offer. However, credit criteria that banks use to approve a home loan application is about 80% similar to one another, so there won't be much variability in credit score's influence even if you ask for quotes from different banks. The only thing you can do is to be careful about how you manage your finances every day so that you can maintain as great of a credit score as your circumstances allow.

Average Fees & Cost of Refinancing

Besides interest rate, there are other costs associated with getting a home loan. Because most Singaporeans refinance their home loans every 2-4 years, it's beneficial to minimise restrictions and fees that prevent you from refinancing like lock-in periods, legal fees, valuation fees and fire insurance premiums, which could eat into your savings in interest.

For instance, consider a home loan of S$500,000. You used to pay 2% of interest, but you are getting it refinanced to 1.5% per year, resulting in S$2,500 in annual savings. However, if you are not careful about fees involved in refinancing, you could potentially end up spending about S$4,000 just in legal fees, valuation fees and early-repayment penalties. Therefore, it's extremely important that your bank offers subsidies for your legal fees. Some banks even provide their in-house valuer for free, which can save you another S$1,000. Below is a list of fees that you need to watch out for, as well as average of these costs that we've observed in the market.

| Fees In Refinancing | Average Cost | Note |

|---|---|---|

| Legal Fee | S$2,500 | Can be as high as S$3,500-S4,000 for homes worth >S$5mn |

| Valuation fee | S$500-S$1,000 | Ranges from S$200 to S$1,500 |

| Fire Insurance | S$120/annum | Some banks pay the 1st year's premiums |

| Partial/Full Redemption Fees | 1.5% | |

| Cancellation Fees | 1.5% | A few bank charge 1% or 2% |

| Pricing Reset Date Penalty | 0.5%-1.5% of amount prepaid |

Read More:

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.