4 Ways That Understanding Your Cognitive Biases Can Save You Money

Even the wisest among us have our weaknesses. Often these weaknesses take the form of cognitive biases, which prevent us from identifying areas for positive changes in terms of our personal finances. In this article, we've outlined some examples of these biases to help you from wasting your own money.

Diminishing Sensitivity & Refinancing Your Home Loan

First, consider the phenomenon of "diminishing sensitivity", which suggests that we are less responsive to changes the further they are from a reference point. Wharton School at the University of Pennsylvania professor Jonah Berger, describes this well in his book "Contagious: Why Things Catch On". Berger conducted a study in which 87% of participants said they'd drive an extra 20 minutes to save $10 on a clock radio normally priced at $35, but not to save $10 for a TV normally priced at $650, even though the savings and time of travel was the same in both scenarios. These findings suggest that certain personal finance optimisations may feel insignificant even if they offer valuable savings.

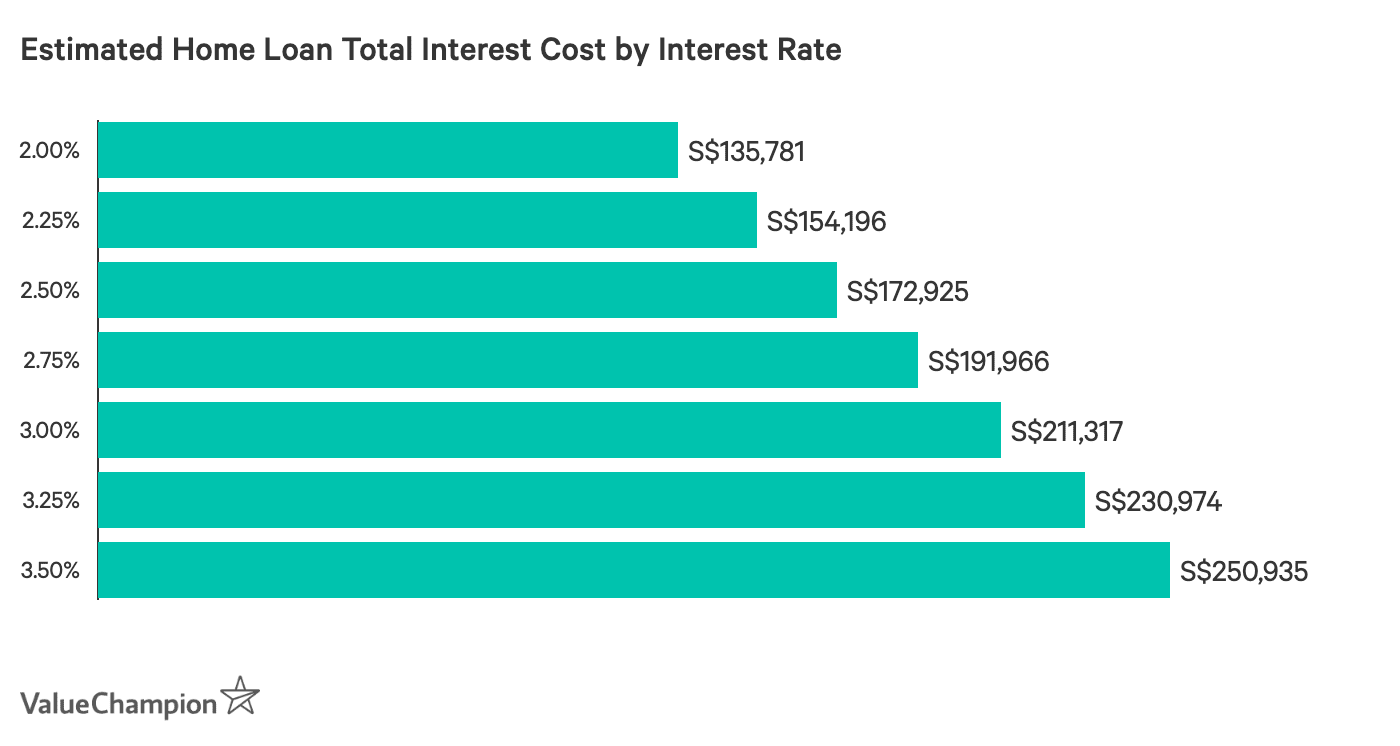

This bias can cause you to waste even more money in some situations. For example, imagine that you have a home loan with an interest rate of 2.5%. If you were able to refinance your loan, you might be able to obtain a lower interest rate, such as 2.25%. To many individuals, this lower rate might not seem like a big deal, given the fact that it is tied to a sizable home loan principal. However, switching to even a slightly lower interest rate can actually save you a lot of money over the course of your loan. For instance, the total interest cost of a 25-year, S$500,000 housing loan with an annual interest rate of 2.5% is S$18,729 higher than the same loan with a 2.25% interest rate. Of course, there are fees associated with refinancing that you'd need to consider, but even seemingly small differences in home loan refinancing rates can result in significant differences in cost.

Loss Aversion & Planning for Retirement

Another interesting finding from behavioural psychology is that humans tend to be irrationally impacted by the prospect of losses compared to those of gains. Nobel Prize winning economist Daniel Kahneman first observed this phenomenon in a coin-flip experiment with his students. After explaining that they would lose $10 if the coin landed as tails, he asked his students how much they would have to win in order to accept the proposition. His students consistently expected $20 if they won the coin flip, or twice a much upside, to accept the deal. This suggests individuals may be more concerned with losses than they are with the opportunity for gains.

This bias can be a hindrance to those planning for their retirement. While it may seem wise to keep your retirement funds in a savings account, you are likely to miss out on significant returns other investments over a long time period. For example, investing in the stock market has traditionally offered much higher average annual returns (7-10%) compared to savings accounts. Alternatively, you can limit your risk profile by diversifying your portfolio or pursuing less risky investments such as bonds, or increase your risk exposure in order to pursue higher returns through crowdfunding investing platforms. With that said, we strongly recommend that you conduct thorough research and develop your own personalized strategy before investing.

Survivorship Bias & University Education

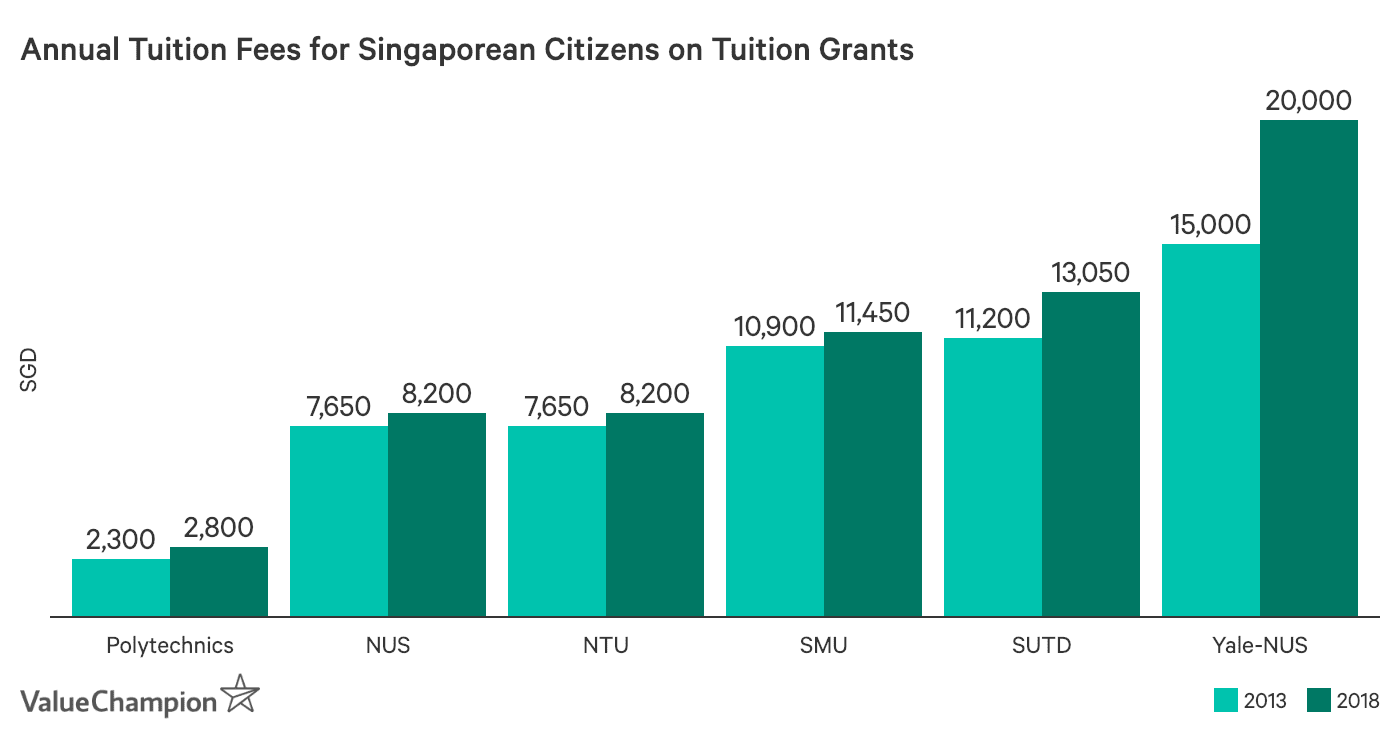

Not only can biases impact our housing expenses and investment decisions, they can even impact career decisions. For example, people often highlight the fact that star entrepreneurs such as Steve Jobs, Bill Gates and Mark Zuckerberg dropped out of college in order to start their successful companies. These examples may make us susceptible the survivorship bias. While those three men did have great success after leaving their universities, they are exceptions and nearly all other dropouts were less successful. While it can be possible and attractive to imagine that you don't need a university degree to be successful, given the rising cost of university tuition, a university degree still offers a relatively high return on investment.

Anchoring Bias & Dealing with Salespeople

Another relevant cognitive bias is known as "anchoring". The anchoring bias is a tendency for individuals to rely heavily on the first piece of information that they encounter. Research by Amos Tversky and Daniel Kahneman found that individuals' estimates for the number of African countries in the United Nations was impacted by the number the participant had just spun on a wheel. This indicates that once we have a number in mind, it adjusts our frame of reference. This can be problematic when shopping for something without conducting prior research. For example, the price first offered by a car salesperson may mentally tether us to a certain price range from the start of negotiations. Therefore, it is important to set your own price expectations for these types of purchases by conducting your own review prior to negotiations.

Be Aware of Your Own Biases to Save Money

Thanks to advances in behavioural psychology, we have an increasingly accurate understanding of our habits and logical limitations. While some of the biases on this list may be more relevant to you than others, it should give you a broad understanding of the types of personal pitfalls that exist. Hopefully you'll be able to make sound financial decisions going forward with this knowledge.